HOME > ジャパトラブログ&ニュース

2020年03月25日

コラム/最適物流の科学㊿

最適物流の科学

弊社社長の菅が、2017年12月に『最適物流の科学―舞台は3億6106万平方km。

海を駆け巡る「眠らない仕事」』という書籍を出版しました。

そこで、本ブログでも、その書籍から抜粋した内容を

毎週1話ずつ、ご紹介していきたいと思います。

第五十回となる今回は、「過当競争の荒波を越えて」というテーマで「手を携え「最適物流」の実現を」をお話しいたします。

↓

↓

——————————————————————————————————–

「手を携え「最適物流」の実現を」

海上運賃の適正化と同時に、各海運業者の関係にも適正化が求められます。荷主の要望に対し柔軟に応えていく上で、事業の多角化は必要なことかもしれません。ただ、いずれの企業もすべての業務を自社で行なうことはできません。自社が得意とする分野以外は外部の事業者に委託するのです。本来の同業者間で競い合うこと自体は否定されるものではないでしょう。しかし、業種の垣根を越えて闇雲に仕事を奪い合う状況は、あまり健全とはいえません。

それよりも各事業者が自社の特徴・強みを生かせる分野にできるだけ特化し、それを伸ばしながら分業化を志向する取り組みが重要ではないでしょうか。一企業が業種の幅を広げて無闇に競争するのではなく、各社がもっと本来の業務に力点を置き、緩やかな連携によって荷主のニーズに応えていくのが理想です。そうした棲み分けを図ることで無駄な部分をなくし、各事業者が業界内で共存していくことも重要だといえるでしょう。

海運業者が多角化する動きは、荷主にとっては歓迎すべき傾向に思えるかもしれません。どの会社に委託してもほぼワンストップで国際物流を担ってもらえるのは便利で、実際そうしたニーズは高まっています。しかし先に述べたように、事業者の違いや特徴がわかりづらくなるといったデメリットを生んでいることも事実です。それ以上に問題なのは、荷主の依頼に対して必ずしも最適な業者に業務委託がなされていないという現状です。

各事業者は、自社でできない業務を他社にアウトソーシングします。このとき多くの事業者は、グループ会社や昔から付き合いのある会社など、自社と近い関係にある業者に発注します。

しかし委託した業者が荷主のニーズにもっとも適しているとは限りません。たとえば倉庫会社の倉庫が最短ルートから離れた場所にあれば輸送効率が悪くなります。運送業者が顧客の貨物に最適なトラックを保有していなければ、安全な輸送に懸念が生じます。内陸輸送と海上輸送の連携が悪ければその分時間を浪費する事態に至ります。

特殊な貨物の場合は、取扱いに不慣れな会社に任せると安全性を十分確保できなくなる恐れがあります。単にその分野の看板を掲げているという点だけでなく、特性・得意分野を見極め、安全性やリードタイム、コストといった要素を考慮し、総合的に委託する会社を選定する必要があるのです。

国際物流業者を選ぶときに考慮するポイントは、第三・四章で述べた通りです。「海外拠点の多さ」、「ネットワークの広さ」、「中立性の有無」を、その重要なポイントとして挙げました。

さらに事業者の実力を判断する基準として、「スペース確保力」、「情報収集力・発信力」、「スピード対応力」の三点を紹介しました。これらの条件を満たす国際物流業者が、最適なプロフェッショナルたちとタッグを組んで貨物を輸送することこそが、「最適物流」なのです。

Realization of “optimal logistics” through joint efforts

The ocean fare is required to be adjusted properly. At the same time, the relationships among shipping companies are also need correction. Diversification of business might be necessary to respond to shippers’ request flexible. Diversification of business might be necessary to flexibly respond to shipper’s request. Still, none of the companies can do their whole businesses by themselves. I propose that companies should entrust outside companies with the exception of the particular fields where they are superior. The idea of competing with the companies that were originally in the same industry should not be denied. However robbing one another of business opporunities beyond the industry borders is not morally healthy.

I believe the important thing is that each company makes efforts to specialize as much as possible in the field where their characteristics and strengths can be manifested. Also important is that they aim to realize the division of their labor while pursuing their strong realms. My ideal is that each company will concentrate on their original business and thus respond to the shipper’s needs by gentle cooperations, instead of simply attempting to expand their businesses and compete indiscriminately. It can be said that the important thing is to reduce wasted efforts and make coexistence and mutual prosperity possible by dividing the responsible business fields in this manner.

The diversification movement of shipping companies may be welcomed by shippers. Whichever shipping company we may choose for international transport, if it could handle everything to the end, that would be so convenient and wonderful. Actually such needs of one-stop operation are increasing. However, as I mentioned earlier, this diversification trend entails the disadvantage that it is difficult to see differences among or characteristics of the shipping companies. Moreover, the outsourced company is not always an optimal choice for the shipper’s request. This is much more problematic.

Companies usually outsource the field that they cannot take care of themselves. When they outsource, they send orders to ta closely-related company or such a company as is in the same group or a long-acquainted company.

However, the outsourced companies are not always best suitable for the shipper’s needs. For example, if the warehouse of the outsourced company is located away from the shortest route, the transportation efficiency is very poor. For example, if the outsourced carrier does not own the optimal truck for the shipper’s cargo, iConcern about safe transportation will arise. For example, if the cooperation between inland transportation and marine transportation is poor, time will be easily wasted.

If the unfamiliar company handles a special cargo, sufficient safety may not be secured. It is necessary to select a company by comprehensively considering the factors such as characteristics, specialty, safety, lead time, and cost. Just knowing the company is in that field is not good enough for this selection.

I described the points to consider in choosing an international logistics agency in chapter 3 and 4. I listed “the number of overseas bases”, “the vastness of the network”, “the existence of neutrality” as its important points.

In addition, I introduced the three points “ability to secure the space”, “information gathering ability / ability to be an origin of information”, “ability to respond to speed” as criteria for judging the competence of the international logistics agency. “Optimal logistics” means the Cargo transport by the international logistics agency that fulfills these requirements and work otgether in rhythm with the most appropriate professionals.

——————————————————————————————————–

ご興味を持っていただけた方、続きを一気にご覧になられたい方は、ぜひアマゾンでお求めください♪

最適物流の科学――舞台は3億6106万平方km。海を駆け巡る「眠らない仕事」

https://www.amazon.co.jp/dp/4478084297/

北米向けコンテナ海上輸送(FCL)のエキスパート!詳しくはこちらから。

工作機械・大型貨物・重量物などのフラットラックコンテナ、オープントップコンテナ海上輸送ならおまかせ!詳しくはこちらから。

コンテナのサイズ表はこちらから。

投稿者

ジャパントラスト株式会社

2020年03月18日

コラム/最適物流の科学㊾

最適物流の科学

弊社社長の菅が、2017年12月に『最適物流の科学―舞台は3億6106万平方km。

海を駆け巡る「眠らない仕事」』という書籍を出版しました。

そこで、本ブログでも、その書籍から抜粋した内容を

毎週1話ずつ、ご紹介していきたいと思います。

第四十九回となる今回は、「過当競争の荒波を越えて」というテーマで「適正運賃が荷主の利益を守る」をお話しいたします。

↓

↓

——————————————————————————————————–

「適正運賃が荷主の利益を守る」

かつて国際定期航路の運賃は、海運業者間の協定によって決められていました。それを行なっていたのが、海運同盟あるいは運賃同盟と呼ばれる国際的なカルテルです。運賃を定めるだけでなく、寄港地を規制したり、新規参入を制限したりすることで過当競争を防いでいました。

しかし一九八〇年代に入ると、同盟に加入しない船会社が現れるとともに、アメリカで規制緩和が進められたことなどにより、同盟は弱体化していきました。その後もEUで海運同盟に対する競争法(独占禁止法)の適用が決まるなど、同盟の力はますます弱まっていきました。こうした経緯で海運同盟が実質的に崩壊したことも、今日のような過当競争を招いた要因としてあげられます。最近の世界的な海上運賃の下落傾向は、「上海発海上コンテナ運賃指数(SCFI:Shanghai Containerized Freight Index)」の推移などを見ても明らかです。

運賃を自由競争に委ねること自体は間違いではありません。あらゆる障壁を撤廃し、新規参入を促すことは経済を活性化させる上で必要です。競争によって運賃が下がり、サービスが向上するのであれば、それは荷主にとって喜ばしい結果でしょう。しかし競争の激化によって船会社自体が疲弊してしまっているのが海運業界の現状なのです。

実際、二〇一六年には韓進海運という大手船会社が破綻するという事態も起きてしまいました。この時荷主は、他の船に貨物を移す必要に迫られ、大きな負担を強いられました。中には航空輸送を使わざるを得なくなり、莫大な費用負担を強いられた荷主も少なくありませんでした。

安い運賃によって利益を享受できても、船会社がサービス停止に追い込まれたり、あるいは合併等でサービスが集約されてしまったりしたら、その都度荷主は、高い費用を払ってでも他の輸送手段を見つけねばならなくなります。船会社の経営状態を心配しながら貨物を委託する会社を選ばねばならない状況は健全とはいえません。リスクを伴う低運賃よりも、安定・安心の可能性が高い適正運賃の方が荷主にとって好ましいのではないでしょうか。

以前、ある船会社で、上海からブラジルまで一コンテナ一〇〇ドルという常識では考えられない運賃の提示がなされました。そこまで極端なレベルの低運賃を望む荷主がいるでしょうか。

運賃競争がこのまま行き着くところまで行った場合、最終的には船会社が一社になることすら現実味を帯びてきます。サービスが一つに集約されることが、荷主にとっての利益といえるでしょうか。「最適物流」も、複数の船会社がさまざまなルートで船を運航させて初めて実現されます。

船会社がここ数十年にわたって繰り返してきたシェア争いも、そろそろ見直す時期に来ているかと思います。業界では、これまでにGRI:General Rate Increase(海上運賃一括値上げ)が何度も試みられてきましたが、いずれも失敗に終わりました。船腹量が余剰している限り、従来のやり方では効果が一時的なものだということは歴史が証明しています。また、近年では日本の海運マーケットは世界一安いともいわれています。これは、船会社と実荷主の直接契約の歴史が長いのも一つの原因であると思います。

なかには、船会社が荷主に運賃を提示する際、「大手荷主だから」、「有名荷主だから」、「付き合いが長いから」といった非経済的な理由で安売りをしてしまうケースもみられます。取引を維持するためにはやむを得ないことかもしれませんが、それは結果として自らの首を絞めるようなものです。

やはり、正確にコストを把握し、適正な利益を乗せた運賃を、どの荷主に対しても提示することが求められます。とはいえ、船会社が実荷主に対して圧倒的に不利な立場にあるという現実がある以上、それまでの慣行を変えるのは難しいことかもしれません。

そこで、一つの解決策として、船会社(実運送事業者)から実荷主には直接スペースを提供せず、フォワーダーにのみ提供する方法を提案したいと思います。フォワーダーが荷主の代わりに全船会社の情報を収集し、交渉をするのです。

船会社が直接に実荷主に営業をする場合、どうしても固定費を少しでもカバーするため船会社の立場が弱くなり、今までの付き合いやネームバリューを重視し、採算度外視で安い運賃を提示しがちです。

そうではなく、スペースをフォワーダーのみに適正運賃で卸し、実荷主に対する営業はフォワーダーに託し、そこで適正な競争をしてもらうのです。フォワーダーは、基本的に船会社からの仕入れ値以下で売ることはありません。自社で船を所有しないためその固定費がなく、スペースが自社の在庫になるわけでもないので、赤字を出すレベルまで安く売る必要はないからです。

また、そうすることで船会社は自社船の運航に専念することができます。同様に、荷主も本業に専念することができます。実際、荷主が全船会社の情報を集め、船会社と直接交渉をするのは容易なことではありません。日本国内で国際物流の情報を広く収集するのは非常に難しいのが現状です。

そうした情報を収集し、提供することこそが、フォワーダーの役割であり、かつ最大の特徴ともいえるでしょう。フォワーダーは、海外にある船会社の本社を直接訪問し、その船会社のプライシング、スペースコントロール担当者と直接交渉し、パイプを構築します。さらには、船会社の役員クラスの人物と会食等を通じての情報収集を行なうこともあります。そうして、日本の船会社の担当者も知り得ない情報を得るのです。

実際エアー業界は、すでにエアーフォワーダーだけにスペースが提供されるスタイルでほぼ運営されています。海運業界でもできないことはないでしょう。また海外では、フォワーダーの方が実荷主に近く、船会社と健全なパートナーシップを結んでいるケースが多く見られます。

船会社は、売っているもの(船のスペース)を在庫にすることができません。買い手に対して圧倒的に不利な立場にある船会社を保護することこそが、「公正な取引」といえるでしょう。先に述べた通り、かつては海運同盟(運賃同盟)という国際的なカルテルがありました。運賃に関して、そうした緩やかな話し合いの場があってもいいのではないでしょうか。

適正価格で商売ができない業界は、いずれ必ず立ち行かなくなります。産業自体も衰退へと向かいます。

日本の海運業の維持・発展のためには、適正運賃の確保に向けた努力も求められるのです。日本の海運業界が最悪の事態に陥らないためにも、公正取引委員会への陳情を含め、何らかの手を打つべきではないかと、私は思っています。

第一章で述べた通り、日本の貿易は九九%以上が船舶によって行われています。日本の生存に欠かせない重要な社会基盤ともいえる外航海運を担う日系企業が、遂に一社に集約されました。一九六〇年代に一二社あった日本の船会社が、約半世紀を経て一社になってしまったのです。

談合や同盟、今では船会社の人間同士の挨拶すら厳禁なのに、合併ならOKなのでしょうか。合併はむしろ同盟よりも立派な〝談合〟になるのではないでしょうか。同盟というゆるやかな話し合いの場があり、複数の船会社が存在することにより、ユーザー側からしたら、運賃の値差があり、競争させることができておりました。サービス内容・価格が全く統一されるより複数の選択肢があったほうが、消費者保護になるのではないでしょうか。

新会社での船出も、決して順風満帆ではありません。外資との競争で将来的にどうなるかわからないという不安を抱きながらの出発です。今後、外航海運を担う日本の船会社がゼロになる可能性は否定できません。

それは、たとえば電力会社がすべて外資になるに等しいことです。もし日本の電力を外資に握られたとしたら、有事の際に日本に電力を供給してくれるでしょうか。日本の海運はそうした危機的な段階に入ろうとしているのです。

船会社は、輸送効率を上げるために船を大型化しました。そしてスペースの供給過剰に陥り利益率が下がりました。続いて業績不振を打開するため合併や買収を進め、アライアンスにより共同運航を実施しました。

同時に外国籍船、外国人船員に運航を委ねるようになりました。こうした一連の動きにより、低運賃が実現される一方で、荷主の利便性は失われていきます。さらには、日本の有事への備えを失うことにも繫がります。この流れは船会社だけでなく、関連業者、荷主、そして一般国民にとっても決してメリットにはならないでしょう。一業界人として、船会社間の競争の緩和を切に望みます。

- Going beyond the wild waves of excessive competitions

Proper fare protects shipper’s profit

Formerly, the international regular route fare was decided on by agreement among shipping companies.

An international cartel called shipping alliance or fare alliance was engaged in this important task. In addition to determining fares, they prevented excessive competition by restricting the call ports and restricting new entrants.

In the 1980 ‘s, the alliance became weakened due to the appearance of the shipping companies that did not join the alliance, and also because of the advancement of the deregulation in the US. Furthermore, the power of the alliance continued to get weakened , due to the new application of the competition law (antitrust law) against the shipping alliance in the EU. The shipping alliance virtually collapsed under these circumstances. This fact is one of the reasons that brought the excessive competition like the one seen today. It is clear that the worldwide marine fare is declining these days. This is conspicuous by looking at the transition of “Shanghai Containerized Freight Index (SCFI)”.

The idea of protecting the fares from free competition is not a mistake in itself. Eliminating all barriers and encouraging new entry is necessary for revitalizing the economy. If the competition reduces freight and improves service, it will be pleasing news for shippers. Shipping companies themselves are getting exhausted due to intensified competition. It is the current status of the shipping industry.

In fact, in 2016, a major shipping company called Hanjin Shipping had collapsed. At that time, the shipper had to transfer the cargo to another ship. Some shippers had no choice but to use air transportation, and not a few shippers were forced to accept a huge cost.

Even if shippers take the profit with a cheap fare, they have to find other transportation methods with high costs each time when a shipping companies are forced to stop the operation or to combine their services due to a consolidation. The situation that shipper has to choose with considering about the managing condition of the shipping company is not proper. The proper fare with high possibility of stability and security than low-cost fare with risk would be better for the shippers.

In the past, one shipping company presented the fare of $100 per container from Shanghai to Brazil. This rate was so outrageous. Does any shipper really want such an extremely low fare?

If the fare competition gets further heated up, it may become realistic that only one company will survive in the shipping industry. Do you think the shipper will benefit if the marine service should be consolidated into one?

“Optimum logistics” is also realized only when multiple shipping companies operate various routes.

It is the time we should review the fight over the market share among shipping companies for the past several decades. In the shipping industry, GRI: General Rate Increase has been attempted many times, but none of them succeeded. History proves that its effect was temporary in the conventional measure as long as the ship quantity is surplus. Besides, the Japanese shipping market is said to be cheapest in the world in recent years. In Japan, the history of direct contracts between shipping companies and shippers is long. This is also one reason why the Japanese marine market can be so cheap.

In some cases, shipping companies present a very cheap fare to the shipper for non-economic reasons such as “You’re a big shipper”, You’re a famous shipper” or “Ours is a long relationship”. Although it may be unavoidable for maintaining trading, it is as if they were inviting a bad result to themselves. In any case, it is required for the shipping company to always grasp the cost exactly and present to every shipper the proper fare that includes its appropriate profits. In reality, shipping companies are overwhelmingly in a disadvantageous position in contrast with shippers. Under such circumstances, it may be difficult for the shipping companies to change their conventional practices.

In this context, as one solution, I would like to propose to shipping companies (real transportation companies) that they should only provide their shipping spaces for forwarders, not to real shippers. Forwarders collect information about all shipping companies and negotiate with them on behalf of shippers.

When shipping companies negotiate with real shippers directly, they much care about the long-term relationship or name value and tend to present cheap fare without much thought of profit. It is because shipping companies somehow try to cover their fixed cost, and as a result, they are in a weak compare position in dealing with actual shippers.

Instead, the shipping companies sell their spaces to only forwarders with the appropriate fare. They commission forwarders to do sales activity, and then forwarders compete properly. Forwarders basically do not sell below the purchase price from shipping companies. It is because forwarders do not own ships, therefore unsold spaces do not become their stocks. That explains forwarders do not need to sell cheaply to the level which generates a deficit.

Accordingly, the shipping companies can also dedicate themselves to operating their own ships. The shippers can concentrate on their main business just as the shipping companies can do so. In fact, it is not easy for shippers to get information from all shipping companies and negotiate directly with shipping companies. Collecting information of international logistics in detail is very difficult currently in Japan.

To collect and provide such information is the role of the forwarder, It can be said that doing so is the biggest characteristics of the forwarder. Forwarders visit the headquarters of shipping companies that is located overseas. They make a strong connection by direct negotiations with the person who takes charge of pricing and space-controlling. Furthermore, it sometimes happens that forwarders collect information by having a kaishoku lunch or dinner with the persons who is in the officer class of the shipping company. Like this, Forwarders may get the information that even the person who represents the Japanese shipping company can not get.

Actually, the air transportation industry is already operated in the manner that almost all spaces are provided only for air forwarders. The marine transportation industry is also able to realize this style. Abroad, there are many cases that forwarders make closer relationships and healthy partnerships with real shippers.

Shipping companies can not stock what they sell (the spaces of the ship). To protect shipping companies in overwhelmingly disadvantaged to buyers is a “fair deal”. As I mentioned earlier, there was an international cartel called the shipping conference (freight union). I suggest shipping companies should be able to have a good discussion opportunity regarding freight.

The industry which people cannot do the business with the proper prices will be doomed to fail sooner or later. The industry itself will surely decline.

Efforts are also required to secure proper fares to maintain and develop the Japanese shipping industry. I think something should be done including a petition to the Fair Trade Commission to avoid Japanese marine shipping industry’s plunge into the worst situation.

As I mentioned in Chapter 1, over 99% of Japanese trade is carried out by ships. Japanese shipping companies are responsible for international shipping, which can be said to be an important social infrastructure that is indispensable for the survival of Japan, The fact is that all the Japanese international shipping companies have been actually consolidated into one company after half a century history of the international shipping industry. In other words,

there were 12 Japanese shipping companies in 1960’s. Today after about a half century, they have become one gigantic company.

Bid rigging or alliance, even greeting people with shipping companies are prohibited in he shipping industry today in Japan. I wonder why consolidation is OK even greetings are severely frowned upon. was no problem? Rather than the alliance, the consolidation could be looked upon as a case of”bid rigging”. Because the alliance can be regarded as gentle negotiation opportunities. When multiple shipping companies are around, the fare differences did occur and they could fairly compete with one another. Natural competetions would be better for protecting consumers by letting them have multiple choices than having them face unified services and prices.

Making a new shipping company is also never promised successno easy challenge at first. It is uncertain if it will do well in the future in competing with foreign capital. It could happen in the future that there will be no more Japanese shipping companies that handle the international shipping. For example, it is almost equal to the situation where all electric companies are managed under foreign capital. If foreign capital take all Japanese electric power, will they supply electricity for Japan at the time of a war? The Japanese shipping industry is about to enter such a critical stage.

Shipping companies have enlarged their ships to increase transportation efficiency. It then caused too much space supply. As a result, the profit margin fell down. Subsequently, shipping companies enforced mergers or acquisitions to overcome their economic slump. They realized cooperative ship operations through alliances.

At the same time, Japanese shipping companies started to entrust foreign ships and foreign crew members to operate them. Through these movements, the low fare was realized, and, on the other hand, shippers had to face inconveniences. In addition, it leads to Japan’s setback in terms of its preparation for a future war. This flow will not benefit not only shipping companies but also related companies, shippers, and the general public. As the person who is involved in the shipping industry, I earnestly wish the competitions among shipping companies will soften.

——————————————————————————————————–

つづく。

次回は、「過当競争の荒波を越えて」というテーマで「手を携え「最適物流」の実現を」をお話しいたします。

ご興味を持っていただけた方、続きを一気にご覧になられたい方は、ぜひアマゾンでお求めください♪

最適物流の科学――舞台は3億6106万平方km。海を駆け巡る「眠らない仕事」

https://www.amazon.co.jp/dp/4478084297/

北米向けコンテナ海上輸送(FCL)のエキスパート!詳しくはこちらから。

工作機械・大型貨物・重量物などのフラットラックコンテナ、オープントップコンテナ海上輸送ならおまかせ!詳しくはこちらから。

コンテナのサイズ表はこちらから。

投稿者

ジャパントラスト株式会社

2020年03月11日

コラム/最適物流の科学㊽

最適物流の科学

弊社社長の菅が、2017年12月に『最適物流の科学―舞台は3億6106万平方km。

海を駆け巡る「眠らない仕事」』という書籍を出版しました。

そこで、本ブログでも、その書籍から抜粋した内容を

毎週1話ずつ、ご紹介していきたいと思います。

第四十八回となる今回は、「日本籍船・日本人船員が激減した背景は」というテーマで「外国籍船が九割以上を占める日本の実情」をお話しいたします。

↓

↓

——————————————————————————————————–

「外国籍船が九割以上を占める日本の実情」

海運業界の現状として、外国籍の船が増加していることにも注目しておく必要があります。船は海上を航行するにあたって、いずれかの国に登録する必要があります。その登録国籍を船籍といいます。序章で二〇一七年六月に起きた衝突事故について記しましたが、その当事者となったコンテナ船ACXクリスタルはフィリピン船籍でした。二〇人の乗務員も同様に全員がフィリピン国籍でした。この例のように、日本の船会社が運航する船でありながら、船籍も乗務員も日本籍でないといったケースは今日では珍しいことではありません。

一九七〇年ごろは、日本商船隊(日本の外航海運会社が運航する商船)のうち、日本籍船は五割を超えていました。しかし、一九七八年には外国籍船の割合が日本籍船を上回ります。その後も日本籍船減少の傾向は続き、二〇〇〇年代に入る頃にはその割合は一〇%を下回る水準にまで減少しました。さらに二〇〇八年には三・七%にまで落ち込みました。

日本商船隊の構成を見ると、国・地域別ではパナマが六一・三%(一五七〇隻)と圧倒的な比率を占めています。次いで日本七・七%(一九七隻)、リベリア五・九%(一五二隻)、シンガポール五・三%(一三七隻)、香港四・四%(一一二隻)などと続きます(二〇一五年)。

日本の船舶法では、日本の船舶はその所有者の住所地に船籍港を置くことが規定されています。しかし、パナマやリベリアといった国にペーパーカンパニーを設立し、そこに船籍を置く場合があります。こうした船を便宜置籍船と呼びます。外国に船籍を置く最大の理由は税金対策です。同時に大きな目的となっているのが、外国人船員を乗せることにあります。日本籍船には日本の免許を持った船員の乗船が義務付けられていますが、外国籍船であればそうした制約を受けません。外国人船員を乗せた方がコストを削減できるため、船会社はそうした選択をしているのです。

便宜置籍船が増えることは、税収、日本人船員の雇用といった点で我が国に不利益をもたらします。また便宜置籍国の海運の発展を阻害するといった問題も指摘されるなど、この傾向に対して批判的な意見が多いことも事実です。とはいえ過当競争が繰り広げられている海運業界において、船会社がコストの高い日本籍船を所有するのは難しいという現実があります。

問われる日本籍船を保持する意味

二〇一一年の東日本大震災に際して、日本の海運業界はその復興支援に大きな力を発揮しました。内航海運業界は震災発生からまもなく対策本部を設置し、業界を挙げて救援物資などの輸送を開始しました。外航海運業界も、日本船主協会と川崎汽船、商船三井、日本郵船の各社が協力し、海外から被災地に向けて物資の輸送を行ないました。

一方で海外の船会社の中には、日本への寄港を回避する動きが見られました。リベリアなどは、福島第一原発事故による放射能漏れへの懸念から、一定距離内の海域での航行回避を推奨する勧告を出しました。ドイツのある船会社は、本社の指示で京浜港への寄港を取りやめました。同様に各船会社の判断で外航船舶の日本への寄港を回避するケースが相次ぎます。さらには、外国人船員が日本船舶への乗船を拒否したり、外国の港で日本の外航船が入港を断られたりするケースもありました。

一連の出来事は、いずれも原発事故に関する風評に起因するものです。正確な情報が伝わると同時にそうした動きは終息に向かいましたが、日本の非常時に際して、諸外国が必ずしも協力的な態度を示してくれるわけではないことを知らされる事象でもありました。

日本が戦争に巻き込まれるような事態が起きた場合は、そうした懸念がさらに高まります。古今東西、戦争の勝敗は兵站(ロジスティック)の構築・維持が左右してきたと言っても過言ではないでしょう。現代の戦争において、軍事物資輸送の主力を担っているのがコンテナ船です。つまり、コンテナ船をどれだけ確保できるかが、国の命運を左右するともいえるのです。

先の太平洋戦争で日本が敗れた要因は、ロジスティクス戦略の欠乏によるところが大きいともいわれています。当時、アメリカの潜水艦は、日本の戦艦を狙わず、輸送船を集中的に攻撃しました。そうすることで、リスクのある戦闘をすることなく効率的に日本の前線兵力を消耗させていったのです。戦争そのものを避けるよう最大限の外交努力をすることが重要であるのはいうまでもありません。しかし、もし万が一戦争という事態に突入してしまった場合のことを考えると、(ここでは多くは語りませんが)かつて太平洋の島々で起きた悲劇的な出来事が二度と繰り返されないよう、やはり兵站を担う輸送船を平時から保持しておくことも欠かせないでしょう。

先に見たように、今日では日本と外国の港を行き来する船の多くが外国籍で、乗務員も外国籍を持つ人たちが多くを占めています。平時においては支障がなくても、想像を超える災害発生時や戦争などの有事に際してそれらの船が日本のために動いてくれるかどうかが強く懸念されます。

政府も日本籍船が極めて少ない状況を憂慮し、さまざまな取り組みを始めています。その一つが、一九九六年に導入された国際船舶制度です。日本籍船のうち国際海上輸送を確保する上で重要な船舶を国際船舶と位置付けて、一定の要件を満たす船舶については海外への譲渡、貸渡に際して届出制・中止勧告制を取るというものです。このような船舶に対しては、税制上の支援措置が講じられます。他にも外国籍船を日本籍船にするための変更手続き(フラッグバック)の見直し、改善に向けた取り組みも進められています。こうした施策により二〇〇九年以後は日本籍船の数が増加に転じ、二〇一五年には七・七%まで回復しています。

海運業者は、荷主の利益を第一に考える必要があります。その前提として、業界内で生き残っていくために、自社の利益を追求することも否定されるものではありません。ただし有事に際しては、事業者が国民全体の利益を最優先に考えることも重要になってきます。

また、万が一国際的な合併等によって、外航海運を担う日本の船会社がなくなったとしても、日系の物流会社が市場をコントロールするだけの力を持ち続ける必要があります。有事に際しては、そうした日系物流会社が存在することも欠かせないのです。

- Background of the sharp decline of Japanese flag ship and Japanese crew

Facts of Japan where foreign vessels account for more than 90% of the ships it operates.

It is also necessary to pay attention to the increasing number of foreign-owned vessels as the current situation of the shipping industry. Ships sailing over the sea need to register in one of the countries. That registered nationality is called a flag country. I wrote in the introduction about the collision accident that occurred in June of 2016. The container ship ACX Crystal was a Filipino flag. Likewise, all 20 crew members were Philippine nationality. As in this example, it is not uncommon today that shipping companies and crew members are not Japanese nationality while being operated by Japanese shipping companies.

Around the time of the 1970s, among Japanese merchant fleets (merchant ships operated by an international shipping company of Japan), Japanese flag ships exceeded 50%. However, in 1978 the percentage of foreign vessels exceeded that of Japanese-flagged vessels. Thereafter, the ships of Japanese flags continued to decrease, and the rate decreased to less than 10% around the time of the 2000s. Furthermore, it fell to 3 ·.7% in 2008.

Looking at the composition of the Japanese merchant fleets, Panama is occupying an overwhelming proportion of 61.3% (1570 vessels) by country and region. Next, with 7.7% of Japan (197 vessels), Liberia 5.9% (152 vessels), Singapore 5.3%(137 vessels), Hong Kong 4.4%(112 vessels) and others (2015).

According to the Ship Law of Japan, it is stipulated that each ship in Japan shall have a port of registration at the address of its owner. However, there are cases where a paper company is established in a country such as Panama or Liberia, and the ship is registered there. These vessels are called convenience vessels. The biggest reason for putting a ship’s flag in a foreign country is for tax protection. At the same time, another main objective is to have foreign seamen on board. Japanese ships are obliged to board the crew with the Japanese license, but if it is a foreign nationality ship, this rule is excluded. The shipping company is making such a choice because it is possible to reduce the cost by putting foreign seamen.

Increasing the number of convenience vessels brings disadvantages to Japan in terms of tax revenue and employment of Japanese seafarers. It is also pointed out that there are many critical opinions against this practice, which causes such problems as impeding the development of maritime transport in conveniently registered countries. However, in the shipping industry where fierce competition is spreading, the reality is that it is very difficult for a shipping company to own a costly Japanese-flagged ship.

What is the meaning to hold Japanese flagged vessels?

On the occasion of the Great East Japan Earthquake of 2011, the Japanese shipping industry showed great strength in supporting its reconstruction. The shipping service industry set up a headquarters soon after the earthquake occurred, and started transporting relief goods, etc. In the international shipping industry, the shipowners’ association and Kawasaki Kisen Kaisha, Mitsui OSK Lines, and NYK Line companies cooperated to transport goods from abroad to affected areas.

Meanwhile, some overseas shipping companies chose to avoid calling in Japan. Liberia and others issued a recommendation to navigation in sea areas within a certain distance due to fears of radiation leakage due to the Fukushima Daiichi Nuclear Power Plant accident. A certain shipping company in Germany canceled the call to Keihin port at the direction of its headquarters. Likewise, at the discretion of each shipping company, there were more cases where foreign shipping vessels avoided calling in Japan. Furthermore, there were cases where foreign crew refused to board Japanese ships, or where Japanese vessels were refused entry at foreign ports.

These series of events are all attributable to rumors about nuclear power plant accidents. After accurate information was conveyed to the world, such movements ended, but we learned from this lessen that Japan’s emergency situation does not necessarily invite cooperative attitudes from other countries.

If a situation such as Japan get caught up in war, that concern will be further raised. It is not an exaggeration to say that in all times the construction and maintenance of logistics crucially influenced the war victories or defeats worldwide. In modern warfare, the container ships have been responsible as the main force of military goods transport. In other words, it can be said that how much you can secure container ships sways the country’s fate.

It is said that the defeat of Japan in the past Pacific War was largely due to the lack of logistics strategy. At that time, the American submarine intensely attacked the transport ships instead of aiming at the Japanese battleships. By doing so, America exhausted Japan’s front line force efficiently without engaging in risky battles. It goes without saying that it is important to make the utmost diplomatic efforts to avoid the war itself. However, considering what will happen if we should go into a major war (I will not say much here) and in order not to repeat the tragic events that once occurred in the islands of the Pacific, it will be indispensable to keep shipping ships for wartime logistics even in the days of peacetime.

As I mentioned earlier, today most of the ships that cross the ports of Japan and foreign countries are foreign flags, and the crew members are also dominated by those with foreign nationality. Even without trouble in peacetime, it is very doubtful whether those ships will move for Japan in the event of an unimaginable disaster or in case of an emergency such as war. Regarding concerns about the situation where the Japanese flag ships are extremely few in number, the government has started various initiatives. One of them is the international shipping system introduced in 1996. Ships that are important in securing international maritime transport among Japanese flagged vessels are regarded as international ships and vessels as long as they meet certain requirements. Their requirements include the duty to report their transfer and lending to overseas countries under the supervision of the Japanese government. For such ships, taxation support measures are taken. We are also reviewing the change procedures (flag back) for making foreign vessels into Japanese-flagged vessels and initiatives to improve them. With these measures, the number of Japanese-flagged vessels began to increase after 2009 and recovered to 7.7% by the year of 2015.

The shipping industry companies need to think first of the shipper’s interests. As a prerequisite, it is regarded as a matter of course to pursue the company’s interests in order to survive within the industry. However, it is also important for operators to consider the interests of the people as a top priority at the time of emergency.

Also, even if there are no Japanese shipping companies that are responsible for international shipping due to international mergers, etc., Japanese logistics companies need to maintain the power to control the market. In case of emergency, it is essential that such a Japanese logistics companies exist.

——————————————————————————————————–

つづく。

次回は、「過当競争の荒波を越えて」というテーマで「適正運賃が荷主の利益を守る」をお話しいたします。

ご興味を持っていただけ高田、続きを一気にご覧になられたい方は、ぜひアマゾンでお求めください♪

最適物流の科学――舞台は3億6106万平方km。海を駆け巡る「眠らない仕事」

https://www.amazon.co.jp/dp/4478084297/

北米向けコンテナ海上輸送(FCL)のエキスパート!詳しくはこちらから。

工作機械・大型貨物・重量物などのフラットラックコンテナ、オープントップコンテナ海上輸送ならおまかせ!詳しくはこちらから。

コンテナのサイズ表はこちらから。

投稿者

ジャパントラスト株式会社

2020年03月06日

遅れに遅れて…(柳)

北米発着の海上コンテナ輸送、全世界へのフラットラック・オープントップコンテナ(オーバーゲージカーゴ)の

輸送を得意としているジャパントラストの柳です。

大丈夫だろうと思ってやってしまいました。(T-T)

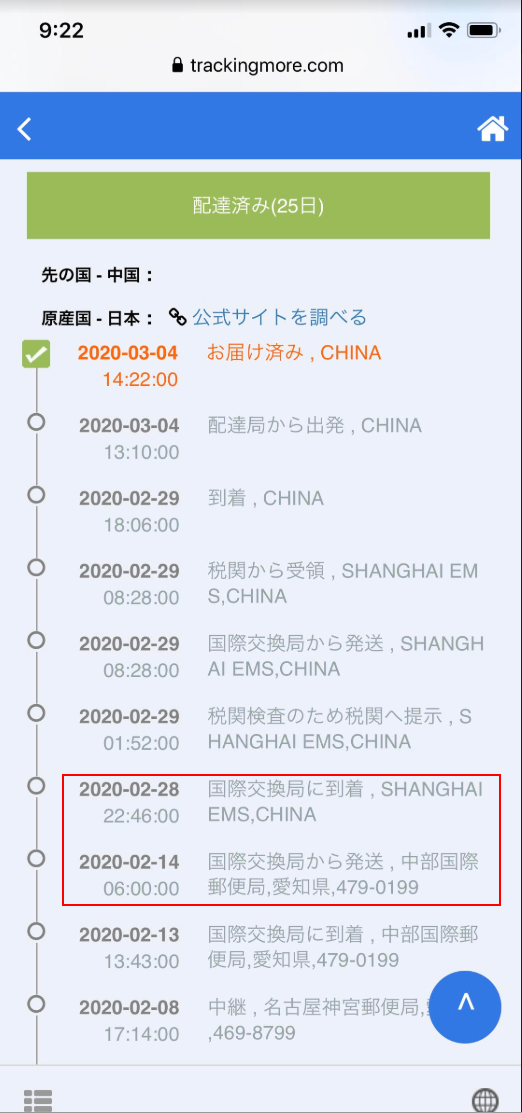

先日、中国の実家に書類一式をEMSで送りました。

ただ、タイミング的に、新型コ●ナウイルスが世の中に影響しはじめた頃で、

確かに、郵便局も「だいぶ遅れて、予定不明」云々の貼り紙もありました。

まぁ!「一般的に、2-3日で到着するから、遅れてもせいぜい7日だろう」と安易に。

結果、下記の通り! ほぼ1か月ほどかかりました。 o(TヘT)o

もちろん、家族にはしっかりと迷惑をかけてしまって、すみません!m(_ _ )m

ちなみに、

赤枠内をご注目、

まるで、書類は日本と中国の間、 まさか空で飛んで14日間もかかったみたい。( ̄▽ ̄;)

とても不可解でした。

(恐らく中国側でデータを反映するのが遅れただろう!)

・北米発着の海上コンテナ輸送でご相談の方はこちら

投稿者

ジャパントラスト株式会社

柳 晶

ジャパントラスト株式会社 カスタマーサービス アシスタントマネージャー 中国出身ですが、「 ロングバケーション」、「 ラブジェネレーション」などのテレビドラマからの影響で、日本が大好きで、振り向けば、好きすぎて来日18年目に立ちました。好きなものは刺身、寿司。嫌いなものは納豆。ジャパントラストでは幾つかの部署を経験しています。

2020年03月04日

コラム/最適物流の科学㊼

最適物流の科学

弊社社長の菅が、2017年12月に『最適物流の科学―舞台は3億6106万平方km。

海を駆け巡る「眠らない仕事」』という書籍を出版しました。

そこで、本ブログでも、その書籍から抜粋した内容を

毎週1話ずつ、ご紹介していきたいと思います。

第四十七回となる今回は、「激しさを増す競争と集約化の流れ」というテーマで「世界的に進展する海運業界の再編」をお話しいたします。

↓

↓

——————————————————————————————————–

「世界的に進展する海運業界の再編」

二〇一七年七月、日本郵船、商船三井、川崎汽船の三社はコンテナ船事業を統合して新会社を設立しました。社名は「オーシャン ネットワーク エクスプレス ホールディングス」。これにより、日本で外航定期航路を持つ船会社は実質一社となりました。新会社の運航コンテナ船は二四三隻、コンテナ積載数換算では約一四四万TEUになり、業界シェアは世界六位となります。

こうした海運業界再編の動きは、日本に限らず世界規模で進行しています。二〇一六年二月、中国遠洋運輸集団(COSCO Group)と中国海運集団(China Shipping Group)が合併し、世界四位の規模となる中国遠洋海運集団(China COSCO Shipping Group)が誕生しました。同年七月には、世界三位のCMA CGM(フランス)がAPL(シンガポール)を買収しました。他にも、最大手のマースク・ライン(Maersk Line、デンマーク)がハンブルク・スード(Hamburg Süd、ドイツ)を、ハパックロイド(Hapag-Lloyd、ドイツ)がUASC(クウェート)を、前述の中国遠洋海運集団がOOCL(香港)を、それぞれが買収する交渉を進めるなど、近年は業界内で大きな動きが相次いでいます。

海運業界では、世界的規模で船会社同士が結びつくアライアンス(同盟)が結成されています。以前は世界一位のマースク・ライン(Maersk Line)と世界二位のMSCによる「2Mアライアンス」、日本郵船や商船三井が加盟していた「G6アライアンス」、川崎汽船などが加盟していた「CKYHEアライアンス」、CMA CGMらによる「OCEANTHREE」といったアライアンスがありました。

近年の合併・買収の動きに伴い、世界の船会社の多くは二〇一七年四月以降、「2Mアライアンス」と「OCEANアライアンス」、そして邦船三社が含まれる「ザ・アライアンス」という三大アライアンスへと集約されました。

目まぐるしく業界再編が進む背景には、海運業界が厳しい不況の波にさらされているという現状があります。これをもたらした一因が、先に述べたコンテナ船の大型化による船腹量の増加です。

輸送効率を上げてコスト削減を追求したことが船腹の供給過剰を招き、それが運賃下落をもたらし、結果として経営を圧迫しています。海運業界は今、こうした悪循環の渦中にあるのです。二〇一六年の韓進海運破綻もその中で起きた出来事でした。

そうした不況の波を乗り越えるため、日本や中国などの大手船会社は、経営規模を拡大して競争力を高めるべく合併という道を選択しました。また船会社同士が世界的規模で提携を深め、業務の効率化を目指そうとする動きの中で、アライアンスは三つに集約されました。

実際、定期航路を構築・運航するには多大なコストが掛かります。各船会社が独自にコスト削減を進めれば競争がより激化し、経営体力の消耗にも繫がります。消耗戦を避けるため、競合する部分を統合して効率化を図るのは合理的な選択だといえるでしょう。また定期航路において、アライアンス内で共同運航を実施し、供給量の調整を図ることも効率アップという点ではやむを得ない決断だといえます。

しかし、こうした動きは必ずしも荷主の利益にはなりません。繰り返しになりますが、合理化によって船の便数が減れば、荷主は不便を強いられます。荷主にとって重要なのは、船の大きさではなく、船の便数の多さです。

寄港頻度が多いに越したことはありません。もちろん、コスト削減によって運賃が安くなるのであれば、それ自体は歓迎すべきことです。しかし、それと引き換えに利便性(寄港頻度)が大きく損なわれる結果はどの荷主も望んでいないでしょう。

競争は業種の垣根を越えて

海運業界で競争が激化しているのは船会社だけではありません。関連業種での競争も年々厳しくなっています。

第三章で見たように、国際物流に携わる事業者は多岐にわたります。実際に船を持つ船会社だけでなく、乙仲、倉庫業者、通関業者など国内物流を得意とする会社や、航空輸送をメインとするエアーフォワーダー、ハードを一切持たないフォワーダーも貨物輸送の委託を受けます。さらに、外資系企業も日本の市場に多く参入してきています。

各社のパンフレットやホームページを見ると、本来専門とする事業以外にさまざまな業務に携わっていることがわかります。これらの企業が業種の垣根を越えてさまざまな業務を請け負うようになった背景の一つとして、政府が進める規制緩和があります。たとえば、第二章で貨物利用運送事業法について触れましたが、この中で第一種利用運送事業については、二〇〇三年の規制緩和により、それまでの許可制から登録制に変更されています。この法改正によって、他業種からの新規参入が容易になりました。他の理由として、業務の多角化によって少しでも利益を増やしたいという事業者側の思惑、ワンストップで委託できる会社を利用したいという荷主側の要望の高まりも挙げられます。

事業者間で健全な競争が生まれ、価格やサービス、利便性が向上するのであれば、こうした傾向は望ましいといえるでしょう。しかし実際は、他業種への参入が過当競争を招き、同時に荷主にとっては事業者の違いや特徴がわかりづらくなるというデメリットを生んでいます。従来は各事業者の棲み分けがある程度、明確になっていました。内陸でのトラック輸送は運輸業者、倉庫での貨物管理は倉庫業者、通関業務は通関業者が担い、フォーワーダーがそれらをコーディネートする役割を果たすという形があり、必要に応じて各社が連携してその関係を維持していました。

それが今では激しく競合する関係に変わってきているのです。

最近は流通業界でも、総合スーパー、ドラッグストア、ホームセンター、コンビニエンスストアなどの垣根がなくなる傾向が見られますが、国際物流業界でも同じような現象が起きているのです。

- Fiercer competition and integration flow

Restructuring of the shipping industry on a global scale.

In July 2001, the three major marine transport companies –

Nihon Yusen, Shosen Mitsui and Kawasaki Kisen Kisen – integrated their container ship businesses and established a new company. The company was named is “Ocean Network Express Holdings”. As a result of this integration, the shipping company that has the regular international navigation routes has just become one company in Japan. Container vessels operated by this new company number 243, the number of the container loading equivalent is about 1,440,000 TEUs, and its industry business share is the sixth place in the world. These shipping industry reorganization movements are progressing not only in Japan but on a global scale. In February 2016, the China Ocean Transportation Group (COSCO Group) merged with the China Shipping Group. As a result, China COSCO Shipping Group, the world’s fourth largest entity, was born. In July of the same year, CMA CGM (France), the world’s third largest, bought APL (Singapore).Besides, Maersk Line (Denmark), the biggest player, acquired Hamburg Süd (Germany), Hapagloid (Hapag-Lloyd, Germany) acquired UASC (Kuwait) and also the aforementioned China COSCO Shipping Group doing negotiations to acquire OOCL (Hong Kong). Recently there have been major moves one after another in the shipping industry.

In the shipping industry, alliances have been formed. As a result, shipping companies are connected with each other on a global scale. In the past, Maersk Line, the world’s No. 1 and No.2 MSC were merged to create the “2MAlliance”, “G6 Alliance” where NYK and Mitsui OSK Lines got affiliated, Kawasaki Kisen united with the “CKYHE Alliance ” and “OCEANTHREE came into existence “by CMA CGM’s merging with others.

Along with recent trends in the form of mergers and acquisitions, since April 1997 many of the world’s shipping companies have been consolidated into the three major alliances, “2 M Alliance”, “OCEAN Alliance” and “The Alliance” which includes three major Japanese companies.

In the background where the industry reorganizations are happening one after another is the current situation that the shipping industry is being exposed to the harsh economic recession. One factor that brought about these consolidations was an increase in the volume of vessels due to the enlargement of the container ships.

Pursuing cost reduction by raising transportation efficiency invites the oversupply of container ships, which results in a decline in freight rates and as a result pressures the management of shipping companies. The shipping industry is now in such a vicious circle. The collapse of the Hanjin Shipping in 2016 occurred in this context.

In order to overcome the waves of such recession, major shipping companies of Japan and China have chosen merging to increase the scale of management and enhance competitiveness. Along this line, the idea of creating alliances was promoted, giving birth to the three giants in the world with aims to deepen global partnership and to improve the efficiency of operations.

Competition goes beyond industrial barriers

In fact, it costs a lot of money to create and operate a regular route. Competition will intensify if each shipping company independently advances cost reduction and it can consume management energies negatively. It may be a rational choice to integrate competing domains and improve efficiency for the sake of avoiding the consumption of unnecessary management energies. Also, it is an unavoidable strategy to try to improve efficiency within the alliance by jointly operating and also by adjusting the supply volume on a regular route.

However, these attempts on the part of the shipping companies do not necessarily benefit shippers. Furthermore, shippers can be inconvenienced if the number of ships is reduced by enlargment and integration. What is important for shippers is not the size of the ship but the number of service or choice.

Of course, if the fare becomes cheaper by cost reduction, it is welcomed by shippers. But they do not want the consequences of great loss of convenience (calling frequency). Competition goes beyond industrial barriers.

Shipping companies are not alone in fierce competition within the shipping industry. Their competition with related industries is getting harder year by year. As we saw in Chapter 3, there are a wide range of business operators engaged in international logistics. Not only shipping companies that actually possess ships but also, companies specializing in domestic logistics, warehouse traders, customs brokers, air forwarders mainly for air transportation, but also forwarders without any hardware, can be commissioned to handle cargo transportation. In addition, many foreign-affiliated companies have entered many Japanese markets.

Looking at the brochure and website of each company, you can see that they are engaged in various fields of business other than their originally specialized realms. One of the reasons why these companies began to undertake various tasks beyond industrial barriers is the deregulation that the government plans. For example, we referred to the Law Concerning the Freight Utilization Transport Business Law in Chapter 2. With regards to Class 1 Utilization Transport Business, the deregulation in 2003 caused a major change from the previous permission system to the new registration system. This legal amendment made it much easier for new entrants from other industries. Other reasons for this legal change were related to the shipping companies’ desire to increase profit even slightly through the diversification of operations and to the shipper’s increasing desire to use the company that can be entrusted with a one-stop service.

Such a trend is preferable if sound competition can be created among business operators and better price, better service and greater convenience are seen there. In fact, however, the entry into other industries invites excessive competition, and at the same time, the shippers experience more disadvantage in discerning the differences and characteristics of business operators. In the past, the responsible realm of each business was clear to a certain extent. Trucking in the inland belonged to the realm of the transport company, cargo management in the warehouse was a warehouse trader’s domain, customs clearance was handled exclusively by the customs broker, and the forwarder played a role of coordinating them. As needed, each company cooperated and maintained the good relationships with other companies.

It is now changing into fierce competing relationships. Recently, even in the distribution industry, there is a tendency for the barriers of comprehensive supermarket, drugstore, home center, and convenience store to disappearn. Similar phenomena are occurring in international logistics industry.

——————————————————————————————————–

つづく。

次回は、「日本籍船・日本人船員が激減した背景は」というテーマで「外国籍船が九割以上を占める日本の実情」をお話しいたします。

ご興味を持っていただけた方、続きを一気にご覧になられたい方は、ぜひアマゾンでお求めください♪

最適物流の科学――舞台は3億6106万平方km。海を駆け巡る「眠らない仕事」

https://www.amazon.co.jp/dp/4478084297/

北米向けコンテナ海上輸送(FCL)のエキスパート!詳しくはこちらから。

工作機械・大型貨物・重量物などのフラットラックコンテナ、オープントップコンテナ海上輸送ならおまかせ!詳しくはこちらから。

コンテナのサイズ表はこちらから。

投稿者

ジャパントラスト株式会社

- ブログ (470)

- コラム/最適物流の科学 (52)

- ニュース (167)

- 2026年5月 (3)

- 2026年4月 (3)

- 2026年3月 (4)

- 2026年2月 (2)

- 2026年1月 (2)

- 2025年12月 (3)

- 2025年11月 (2)

- 2025年10月 (2)

- 2025年9月 (3)

- 2025年8月 (2)

- 2025年7月 (4)

- 2025年6月 (3)

- 2025年5月 (4)

- 2025年4月 (4)

- 2025年3月 (4)

- 2025年2月 (4)

- 2025年1月 (4)

- 2024年12月 (3)

- 2024年11月 (2)

- 2024年10月 (2)

- 2024年9月 (4)

- 2024年8月 (5)

- 2024年7月 (5)

- 2024年6月 (5)

- 2024年5月 (4)

- 2024年4月 (5)

- 2024年3月 (6)

- 2024年2月 (3)

- 2024年1月 (3)

- 2023年12月 (5)

- 2023年11月 (4)

- 2023年10月 (3)

- 2023年9月 (4)

- 2023年8月 (4)

- 2023年7月 (3)

- 2023年6月 (3)

- 2023年5月 (4)

- 2023年4月 (4)

- 2023年3月 (4)

- 2023年2月 (4)

- 2023年1月 (3)

- 2022年12月 (3)

- 2022年11月 (3)

- 2022年10月 (4)

- 2022年9月 (3)

- 2022年8月 (4)

- 2022年7月 (9)

- 2022年6月 (6)

- 2022年5月 (8)

- 2022年4月 (6)

- 2022年3月 (7)

- 2022年2月 (5)

- 2022年1月 (6)

- 2021年12月 (3)

- 2021年11月 (8)

- 2021年10月 (5)

- 2021年9月 (4)

- 2021年8月 (7)

- 2021年7月 (4)

- 2021年6月 (4)

- 2021年5月 (6)

- 2021年4月 (3)

- 2021年3月 (5)

- 2021年2月 (2)

- 2021年1月 (6)

- 2020年12月 (4)

- 2020年11月 (3)

- 2020年10月 (3)

- 2020年9月 (6)

- 2020年8月 (1)

- 2020年7月 (2)

- 2020年6月 (3)

- 2020年5月 (4)

- 2020年4月 (6)

- 2020年3月 (5)

- 2020年2月 (6)

- 2020年1月 (5)

- 2019年12月 (5)

- 2019年11月 (4)

- 2019年10月 (7)

- 2019年9月 (6)

- 2019年8月 (3)

- 2019年7月 (3)

- 2019年6月 (2)

- 2019年5月 (6)

- 2019年4月 (7)

- 2019年3月 (5)

- 2019年2月 (7)

- 2019年1月 (3)

- 2018年12月 (2)

- 2018年11月 (2)

- 2018年10月 (1)

- 2018年9月 (1)

- 2018年8月 (3)

- 2018年7月 (2)

- 2018年6月 (4)

- 2018年5月 (1)

- 2018年4月 (3)

- 2018年3月 (3)

- 2018年2月 (6)

- 2018年1月 (1)

- 2017年12月 (1)

- 2017年11月 (6)

- 2017年10月 (2)

- 2017年9月 (4)

- 2017年8月 (4)

- 2017年7月 (1)

- 2017年6月 (5)

- 2017年5月 (3)

- 2017年4月 (5)

- 2017年3月 (1)

- 2017年2月 (3)

- 2017年1月 (7)

- 2016年12月 (4)

- 2016年11月 (4)

- 2016年10月 (7)

- 2016年9月 (7)

- 2016年8月 (7)

- 2016年7月 (7)

- 2016年6月 (6)

- 2016年5月 (6)

- 2016年4月 (2)

- 2016年3月 (6)

- 2016年2月 (11)

- 2016年1月 (6)

- 2015年12月 (5)

- 2015年11月 (5)

- 2015年10月 (5)

- 2015年9月 (8)

- 2015年8月 (8)

- 2015年7月 (8)

- 2015年6月 (9)

- 2015年5月 (3)

- 2015年4月 (3)

- 2015年3月 (8)

- 2015年2月 (6)

- 2015年1月 (2)

- 2014年12月 (5)

- 2014年11月 (5)

- 2014年10月 (6)

- 2014年9月 (5)

- 2014年8月 (7)

- 2014年7月 (4)

- 2014年6月 (7)

- 2014年5月 (3)

- 2014年4月 (6)

- 2014年3月 (3)

- 2014年2月 (6)

- 2014年1月 (3)

- 2013年12月 (2)

- 2013年11月 (6)

- 2013年10月 (3)

- 2013年9月 (5)

- 2013年8月 (5)

- 2013年7月 (4)

- 2013年6月 (2)